Stock Market Bottoms Don't Require Capitulation but it Sure Does Help

One of the advantages of getting older is experience and the wisdom that (supposedly) comes with it. I would say that over 30 years of playing 'The Greatest Game' would qualify me as an experienced investor. While the education process hasn't always been fun, I have seen lots of different type markets and I've learned a lot from both the bear markets and the bull markets not to mention quite a bit from history books. Those who don't study market history are doomed to repeat the painful parts of it, in my opinion.

Lately, I've heard many pundits calling for a bottom to the stock market collapse and and I've heard just as many calling for the end of economic civilization as we know it today. The truth of the matter is that nobody can perfectly predict the future although some investors are clearly better than others at weighing the preponderance of the evidence and making probability based investment decisions. The best investors I've known are not generally the ones that call market or stock direction the best, rather they are the best managers of risk. Please reread that last sentence because it is the closest thing to an absolute truth that I've seen in 30 plus years in this game.

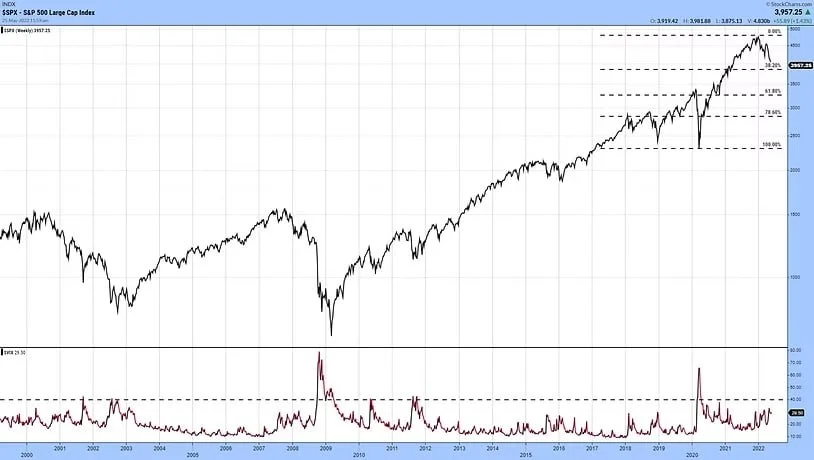

The chart below shows the S&P 500 along with the VIX plotted below it. Spikes above the dotted line at 40 in the bottom pane have generally signalled climatic action coinciding with significant market bottoms.

Let me be clear that for now, with the information that I have today, I think US equities are still in a secular bull market and I haven't wavered on that at all. But the story that seems to be making the rounds in the financial press lately is that there has been no capitulation and that the stock market can't bottom without capitulation. According to Investopedia, "Capitulation in finance describes the dramatic surge of selling pressure in a declining market or security that marks a mass surrender by investors. The resulting dramatic drop in market prices can mark the end of a decline, since those who didn't sell during a panic are unlikely to do so soon after. Capitulation typically follows significant downturns in price, which can take place even as many investors remain bullish. As the downturn accelerates, it reaches a point where the selling by the investors unwilling to suffer further losses snowballs, leading to a dramatic plunge in price."

But the stock market can do anything it wants, with or without capitulation. Consider the following from Anatomy of the Bear by Russell Napier. "The 1982 bear market is again marked by the absence of a final slump in stock prices on high volumes. The great final slump in prices on high volume was as absent in 1982 as it was in 1921,1932, and 1949. The belief in the necessity of such an episode discouraged some investors in 1982. Alfred E. Goldman, of A.G. Edwards & Sons, stated that in the absence of such high volume selling in the market's final decline indicated that the bear market was not over. Ten days after the rally began, Richard McCabe of Merrill Lynch doubted the sustainability of the market rise in the absence of the capitulation event." Well the history books are closed on that chapter as the great bull run of the 1980s and 1990s was just getting warmed up -without capitulation.

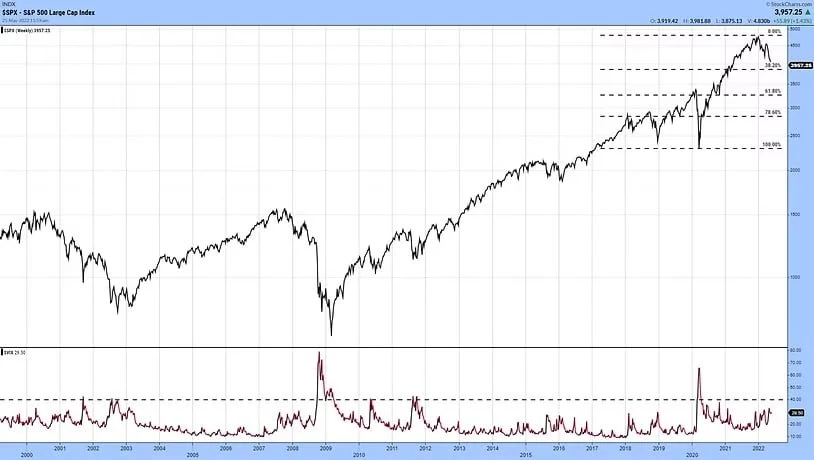

Notwithstanding the above caveat, I do think that it is at least noteworthy that investors currently don't appear to be at that emotional stage of fear that comes with the get me out at all costs panic that sometimes marks important market bottoms. There are lots of ways to measure sentiment to determine whether main street has 'capitulated' and many of those measure are indicating just that. The ever popular VIX index, also known as the fear index, seems to be getting a lot of airtime right now because it hasn't risen above the magic level of 40 that many depend on to mark important bottoms. Because the VIX is receiving so much attention, maybe it won't work this time. But this lack of a convincing bottom is starting to feel like the tech meltdown that occurred over about a two and a half year period starting in the year 2000. That bear market saw the major US Equity Indices drop by over 50% and the tech heavy Nasdaq drop by over 80%. By our count there were at least four counter trend bounces of 30% or more that were not THE bottom during that vicious bear mauling. Therefore, we feel that it is best to wait until a true bottom appears to have been established before aggressively making financial bets.

Four bounces of greater than 30% occurred during the Tech Wreck before THE bottom was ultimately in place.

Let me be clear that to say that stocks will experience a similar outcome to that of 2000 bear right now would be reckless at best. But if we do have a bottom without the aforementioned capitulation, our biggest fear is that bounces will be similar to those experienced during the Tech Wreck, in large part because according to our interpretation stocks just signaled a Dow Theory Sell Signal. That is a subject for another report though. In short, even after the magnitude of this selloff and the attempted bottoming action of late which could prove to be The bottom, risk management is of paramount importance. But isn't it always?