A Shift Beneath the Surface (Quarterly Investment Update)

The first quarter of 2026 marked a clear shift in market character. After a strong start to the year, markets were forced to recalibrate as geopolitical tensions in the Middle East caused oil prices to spike. Higher energy prices renewed concerns about inflation and raised the risk of an economic slowdown, as higher commodity prices can act much like an interest rate hike. Higher gas and oil prices can also contribute to potential inflation, so the dreaded “stagflation” is starting to appear in the headlines. The result was that the S&P 500 declined approximately 4% during the quarter, with more pronounced weakness in technology and other growth-oriented areas, while interest rates moved higher and market participation narrowed. At the same time, leadership shifted meaningfully, with strength concentrated in energy, materials, and more defensive areas of the market. That type of rotation—away from growth and toward defensive or inflation-sensitive sectors—is something we tend to see later in a market cycle. It’s the type of clue that we look for when analyzing the potential for volatile markets.

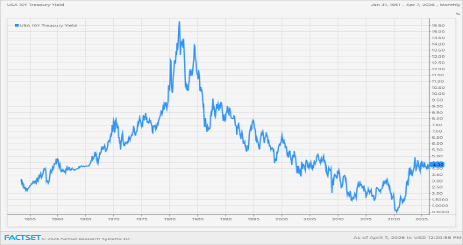

Interest rates likely bottomed during COVID, when the 10-year Treasury reached an intraday low of approximately 0.39%. While rates may fluctuate from here, the long-term trend of declining rates that supported both equity and bond markets for decades is most likely behind us. If that is the case, it represents a meaningful change in the investment environment. Higher energy prices, renewed concerns about inflation, and rising interest rates—potentially exacerbated by geopolitical conflict—create a very different backdrop than what investors have experienced since the stock market bottomed in 2009.

Importantly, this also has implications for portfolio construction. Bonds have historically provided both income and diversification, particularly during periods of equity market stress. In a rising or more volatile rate environment, that relationship may be less consistent than investors have come to expect, which makes diversification across asset classes—and sources of return—more important. That shift in the macro environment is central to how we are currently thinking about markets.

Secular vs. Cyclical Markets

Long term clients of ours should be familiar with our investment thesis that US Equities have been in a secular bull market since the end of the Great Recession. It is our view that markets move in long-term secular cycles, with shorter-term moves along the way. The challenge is that you don’t know in real time whether a downturn is simply a short-term correction or the beginning of something more significant. It is too early to say that we are in a cyclical bear market, and therefore far too early to say that a secular bear market is underway. Those distinctions are only clear in hindsight, which means we have to make decisions before there is certainty.

We use technical analysis as a cornerstone of our risk management process. The market broke below its 200-day moving average on March 19 and remains below that level as of this writing, which typically signals a shift in trend. If the market were to regain and hold that level, we would become more optimistic that this is simply a cyclical pullback. This is a news-driven environment, and conditions can change quickly, so we remain willing to adjust as the evidence changes. The burden of proof, however, remains on the market.

The more important level is the 200-week moving average, which reflects the long-term, secular trend. With the S&P 500 closing the quarter at approximately 6,484, a move toward the 5,200 range which is the current level of the 200-week moving average, would represent a meaningful decline. We are not willing to wait for that kind of drawdown before adjusting positioning. Spending time below current levels increases the likelihood that longer-term support levels are tested, and that is something we are watching carefully.

Whether this becomes a more prolonged issue will likely depend on how geopolitical events unfold—particularly the duration of the conflict involving Iran and the stability of the Strait of Hormuz. A prolonged disruption would likely reinforce higher energy prices, continued inflation pressures, and upward pressure on interest rates.

At the same time, it’s important to distinguish between market weakness and systemic risk. Inflation can drive weaker markets, but more severe downturns are typically associated with stress in the banking system or credit markets. At present, we do not see evidence of that. Concerns around private credit, in our view, are often overstated and not well understood, and we do not currently view that area as a source of systemic risk in the broader market. The stability of the banking system remains an important counterbalance.

None of this is a prediction. It is an assessment of risk.

How We Are Positioned

Our job is not to predict outcomes, but to manage risk as conditions evolve. Our approach is built on a disciplined playbook that allows us to adapt to changes as they occur.

At the asset allocation level, portfolios are structured to align with long-term objectives while maintaining flexibility. Within equities, we emphasize sector rotation and relative strength, allocating toward areas showing leadership and avoiding persistent laggards. Our recent shift toward energy, materials, and defensive sectors reflects that approach. However, we are not completely abandoning the AI trade at this time either.

On the fixed income side, we currently favor U.S. Treasuries, high quality municipal bonds and shorter-duration investments, as managing duration risk becomes more important in this environment. We also believe alternative investments can provide an additional layer of diversification for appropriately accredited investors, particularly when traditional relationships between stocks and bonds are less reliable.

The chart above shows 10-year treasury yields since the 1950s. Rates peaked in 1981, bottomed in 2020 and a new cycle appears to have started.

Given current conditions, we are holding elevated levels of cash. This is not a reaction to headlines, but a result of honoring our stops and managing market conditions. We did not decide to go to a particular cash allocation; we simply ended up here by following our playbook. Extra cash gives us flexibility if conditions improve and protection if they deteriorate. In practical terms, it does mean we are somewhat more cautious today while remaining ready to become more constructive as the market proves itself.

Looking Ahead

There are several ways this could play out. We think that if the situation in Iran and the Strait of Hormuz resolves itself quickly and definitively then markets could rebound quickly. Alternatively, if this lingers on, the current environment could evolve into something more prolonged and challenging. It is too early to draw that conclusion, but not too early to recognize the possibility.

Final Thoughts

Periods like this are where discipline matters most. Markets rarely provide clarity at turning points, and waiting for confirmation often means reacting after the fact. Our focus remains on managing risk, preserving capital, and adapting as conditions evolve. If you have any questions or would like to review your portfolio, please let us know.

Emerald Asset Management is an independent, boutique Registered Investment Advisory firm based in Rocky Mount, NC, serving successful executives, business owners, and high-net-worth individuals across Raleigh, Durham, and Chapel Hill. As a fiduciary-led firm with over 30 years of experience, Emerald provides research-driven investment management and strategic financial planning. The firm specializes in individually managed stock and bond portfolios, alternative investments, and risk management strategies. With a disciplined approach and a commitment to clarity, Emerald helps clients navigate complex financial decisions with confidence. They can be reached at (252) 443-7616 or on the web at www.emeraldam.com.

The information presented is based on sources believed to be reliable and accurate at the time of publication. This material is for educational purposes only and does not necessarily reflect the views of the author, presenter, or affiliated organizations. It should not be construed as investment, tax, legal, or other professional advice. Always consult a qualified professional regarding you

Emerald Asset Management is an investment adviser registered with the U.S. Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about Emerald Asset Management's investment advisory services can be found in its Form ADV Part 2 and/or Form CRS, which is available upon request.